Under any taxation law, the first compliance that a taxpayer is required to fulfill is to get himself registered before the appropriate tax authorities. All the taxpayers are identified from the unique number allotted to them by the concerned tax authorities at the time of obtaining registration. A formal registration with the concerned tax authorities confer the following benefits to a taxpayer:

- Completion of registration procedures formally recognizes a taxpayer as supplier of goods/services;

- A registered taxpayer is formally entitled to collect taxes from his customer and pass on the credit of such taxes to the purchaser/recipient on goods/services supplied to them.

- The intention of government to allow seamless flow of input tax credit from suppliers to recipients at pan-India level can be achieved only if the concerned taxpayers have got themselves registered formally.

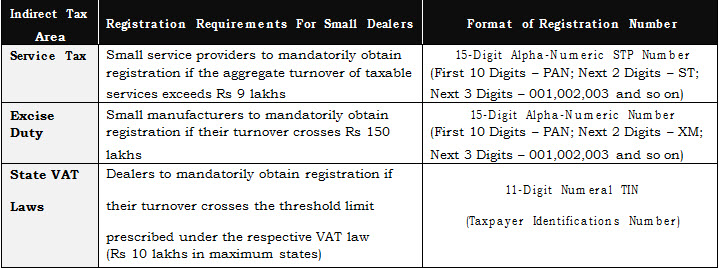

Registration Requirements Under Existing Indirect Taxes Law:

Format of GST Registration Number:

The supplier of taxable supply has to register in each of the state or Union Territory from where the supply has been effected i.e. the registration in GST is PAN based and state specific. Upon registration, the supplier is allotted a 15-digit GST identification number called “GSTINâ€Â. The format of GSTIN is:

(There is a single registration for all the taxes i.e. CGST, SGST/ UTGST, IGST and cessess i.e. Registration under GST is not tax specific but PAN based state specific)

Registration Requirements Under GST Law:

The provisions relating to registration have been incorporated u/s 22 to 30 of the Central Goods & Services Tax Act, 2017 (hereinafter referred to as “CGST Actâ€Â). From a commercial point of view, registration can be classified in the following broad categories:

- Mandatory registration if threshold limit (i.e exemption list) is crossed;

- Mandatory registration even if threshold limit is not crossed;

- Mandatory migration of persons already registered in the present law;

- Voluntary registration;

- Establishment of distinct person;

- Registration for business vertical, etc.

(Some other types of registrations have also been provided for under the GST law but we have decided to skip them considering their limited applicability and scope)

Time Limit For Obtaining Registration:

Every person who is liable for registration has to apply within 30 days from the date on which he becomes liable for registration, in such manner and subject to such conditions, as may be prescribed.

Further, every person who makes a supply from the territorial waters of India shall obtain registration in the coastal State/UT where the nearest point of the appropriate base line is located.

Category 1 – Mandatory Registration If Threshold LimitIs Crossed.

Section 22 of the CGST Act requires a supplier to obtain registration in the State/UT from where he makes a taxable supply of goods and/or services if his “aggregate turnover†in a financial year exceeds the following amounts:

- Rs 10 lakhs in case of eleven special category states (i.e, Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, J&K, Himachal Pradesh and Uttarakhand)

- Rs 20 lakhs in case of any other state.

The term “aggregate turnover†has been defined to include all supplies made by a taxable person, whether on his own account or made on behalf of his principals. To under this meaning better, an illustration has been given below:

Illustration: Mr X makes a supply of Rs 8 lakhs on his own account and he also acts as an agent on behalf of his principal Mr A. On behalf of his principal, he makes a turnover of Rs 13 lakhs. Hence, his total supply would be aggregated to Rs 21 lakhs and he would be liable to get himself registered.

Section 23 of CGST Act permits the following two persons to operate their business without taking registration. In other words, in the following two cases, registration is not required:

- A person exclusively engaged in the business of supplying goods/services that are not liable to tax or are wholly exempt from tax; and

- An agriculturist, to the extent of supply of product out of cultivation of land.

Category 2 – Mandatory Registration Even If Threshold Limit Is Not Crossed.

In the following cases, compulsory registration is required irrespective of the level of turnover:

- Person making inter-state taxable supplies;

- A person receiving supplies on which tax is payable by recipient on reverse charge basis;

- A person who supplies goods/services on behalf of some other taxable person (i.e an agent of some principal);

- E-commerce operators, who provide platform to the suppliers to supply through it (i.e online portals such as Flipkart, Snapdeal, Amazon, etc);

- Suppliers who supply through an e-commerce operator;

- Those ecommerce operators who are notified as liable for GST payment u/s 9(5) (i.e aggregators such as Uber, Ola, etc);

- TDS Deductor;

- Those supplying online information and data base access or retrieval services from outside India to a non-registered person in India;

- Casual taxable person who is not having a fixed place of business in State/UT from where he wants to make supply; and

- Non-resident taxable persons who are not having a fixed place of business in India.

Difference b/w Casual Taxable Person & Non-Resident Taxable Person:

Let us understand this with the help of an example. Let us say a trade fair is being organized in New Delhi. Dealers who carry their business in other states of India and who don’t have a place of business in Delhi set up a stall in the trade fair and sells goods from such stall. Such dealers would be regarded as causal taxable person in Delhi. Further, some dealers from foreign countries who don’t have any place of business in India also set up a stall in the trade fair whereby they exhibit their products and sell the same to the customers. Such foreign dealers who don’t have any place of business in India would be regarded as non-resident taxable person. A casual taxable person or a non-resident taxable person has to apply for registration within 5 days prior to the commencement of business. The registration certificate obtained by such dealers is valid for the period specified in the registration application or 90 days from the effective date of registration, whichever is earlier. The officer may extend the period of 90 days. Such persons are required to make taxable supplies only after receipt of registration certificate and also required to deposit GST in advance equivalent to the estimated amount of tax liability of such person for the period for which registration is sought or for the extended period.

Category 3 – Mandatory Migration Of Persons Already Registered In The Present Law:

Every person who holds a valid registration under the existing indirect taxes needs to get himself migrated to GST law as per the requirements of the CGST Act.

Category 4 – Voluntary Registration:

A person who is not compulsorily require to obtain registration u/s 22 to 24 of the CGST Act may get himself registered voluntarily and all the provisions of the GST law shall apply to such person as if he is a registered taxable person.

Category 5 – Establishment Of Distinct Person:

Where a person has obtained/required to obtain registration in any State/UT in respect of an establishment and such person has another establishment in any other State/UT, such establishments shall be treated as establishments of two distinct persons for the purposes of GST law and both the establishments shall be required to be registered separately.

Illustration: A businessman has a head office in Delhi and he has a branch office in Mumbai and goods are supplied to various customers from the head office as well as the branch office. In such a situation, both the head office and the branch office are to be registered separately under the Delhi SGST & Maharashtra SGST law respectively.

Category 6 – Registration For Business Vertical:

Generally, only a single registration is required for one State/UT. However, Section 25 of the CGST Act provides a dealer an option to obtain separate registrations for each “business vertical†of a person in a State/UT. Business vertical has been defined to mean a distinguishable component of an enterprise that is engaged in supplying an individual product/service or a group of related products/services and that is subject to risk and returns that are different from those of other business verticals.

Illustration: A company is engaged in manufacturing and sale of two products – shoes and shirts. Both the products are managed by their respective divisions and there is no common commercial link between the two divisions. The company, at its option, can obtain two different registrations for the two divisions.

Registration is the most fundamental requirement for identification of tax payers under GST. Without registration, a person can neither collect tax from his customers nor claim any input tax credit of tax paid by him.

About The Author: CA Priyanka Jain

B.Com (Hons) from Shri Ram College of Commerce, Delhi University and a qualified Chartered Accountant and Company Secretary. Presently, working as a Consultant in M/s. S.R. Dinodia & Co. LLP, a reputed taxation firm from New Delhi and providing regular advice to multinational and domestic clients across all areas of taxation, ranging from advisory and transaction structuring to compliances and litigation.